In January 2021, Nowlake Technology was newly established, becoming the parent company of Westlake Services, which operates a used car finance business in the U.S., and Nowcom, which develops and sells systems for automobile dealers and other automobile finance-related products.

LOS ANGELES – The iPhone has an unlikely use.

Among car buyers, an owner of an Apple smartphone is a lower credit risk for automobile loan providers than a person with an Android-based one. Another insight is that people who purchase purple cars are riskier than beige car buyers – but one might have guessed that without the help of artificial intelligence crunching tons of data.

Those are just a couple of the findings that Westlake Financial Services has gleaned by analyzing internal and external auto-loan and borrower data, including proprietary data going back three decades. These types of insights have enabled the Los Angeles-based firm to become the largest provider of auto financing to independent used car dealerships and fifth biggest overall for pre-owned autos in the U.S.

While a fragmented market, with no single lender having more than a 10% share, it’s a massive one with a $1.2 trillion used-car loan balance in 2018. That market is less susceptible to economic downturns too, as owning a car is key in most of the U.S. to get to work, take your kids to school or shop for groceries.

Westlake, which has leveraged its technology – such as using AI long before it became today’s buzzword – efficiency and scale, has racked up a 40% return on equity, twice most of its rivals, and 20%-plus annual growth. It’s slashed overhead costs, as a percentage of its managed loan portfolio, from 11% in 2008 to 2.7% today, while rivals are still many times that.

“AI and machine learning are concepts you hear a lot. We actually do practice them here. We take large sets of data and train the model to do certain predictions – to have a prediction of credit loss, and we price towards that,” says Westlake Group President Ian Anderson. “We look at all of this data each and every day to try make decisions that grow our most profitable business or tighten our least profitable side of the business.”

The company provides consumer auto loans – 95% for pre-owned vehicles, including a major subprime business of people with poor credit – and financing for dealer inventory. Westlake’s number of borrowers in the near prime and prime market of those with better and the best credit is increasing. It also packages car loans that it originated itself, as asset-backed securities, and sells them to major institutional investors in billion-dollar tranches.

In 2011, Tokyo-based trading company Marubeni Corporation took a 20% stake (later raised to 24%) in Westlake, which is part of the Hankey Group. The Hankey family, led by Westlake Chairman Don Hankey, owns 67% and employees hold the remaining 9%.

High-Tech Drives Performance

Gaining the kind of insight seen for instance in the iPhone example doesn’t come easy or overnight.

Westlake vets loans based on its own proprietary credit scoring and loan system, using its own data, some going back decades, and other data from third-party vendors, including FICO scores. Coupled with a petabyte of internal data, which is many times that of rivals, and information that rivals don’t look at like driving records, the firm approves at least 95% of the applications it receives, Anderson says.

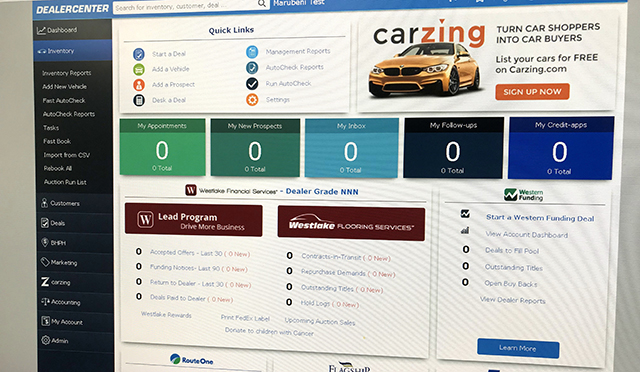

That system was developed internally just upstairs from Westlake’s headquarters. With over 700 employees in the U.S., India and the Philippines, NOWCOM, a Westlake sister company, developed a unique dealer management software, “DealerCenter,” which runs a risk management system developed by Westlake called the “Buy Program.”

“I would be willing to say that we spend double of what our competition spends on technology, including infrastructure like databases and cloud systems. We spend a lot on technology to save a lot on processes, like loan origination, processing car titles, mail and income verification. That’s made us a much more efficient company and one with a much lower operating cost,” he says.

Car Buyers Excited … Until They’re Not

But what does all that high-tech mean to dealerships and customers?

Zain Haroon, the finance manager at North Hollywood Toyota, says that helps dealers sell cars and bolster their bottom line, and it gets buyers into a ride that fits their needs – and quickly. (Owned by the Hankey Group, the North Hollywood Toyota dealership is one of Toyota Motor’s largest in the U.S. by sales, with some 450 to 500 new and used cars sold every month.)

In addition to getting loans checked within seconds, DealerCenter enables the finance staff to quickly adjust loan parameters if it’s not getting a green light. (DealerCenter, among other things, also manages inventory and customer information.) With a few mouse clicks, staffers can adjust factors like the down payment and model of car, choosing from the dealer’s new and used inventory. Other lenders don’t offer that instant flexibility if an application is rejected, Haroon says. They require him to call and try to rehash the deal, which takes critical time – time during which the buyer might get cold feet.

“Buying a car for anybody is exciting. People are nervous. The biggest purchase is their home and the second is usually their car. While you are sitting here, spending two hours figuring out what to do, the customer, at that point, might not want to buy the car anymore. They’re not excited anymore,” he says. “It’s all about the excitement. We create excitement. Time is everything, and Westlake provides that.”

Wooing Each Other

“The first talks between Westlake and Marubeni, right after the 2007-2008 U.S. financial crisis and subsequent recession when Westlake was looking for capital, didn’t bear fruit. But the two inked an agreement in 2011, even after that financial need had vanished, once financial markets thawed out,” Hankey says.

“As I got to know Marubeni, I thought it might be good for our company to get someone more worldly than us, and maybe would help us come up a notch. And I think it did that. It was a big help to us,” he says.

While offering Westlake advice or reassuring it on its decisions, Marubeni’s backing ensures that it won’t be strapped for cash when a business opportunity pops up.

“Short on capital, you don’t grow too much. If you sit there and you have another $100 million in capital – ‘oh, here’s something we can do, here’s another company we can buy, here’s another area we can penetrate to try and increase our sales.’ Having a partner like Marubeni always allows us to grow and to expand,” he adds.

For Marubeni, which is mainly a B-to-B operation, partnering with Westlake offered the opportunity to gain knowledge about the consumer car loan business – something that it could leverage in other markets outside the U.S.

“There’s a lot of talk today about Big Data, but Westlake was working with data from way back and is really adept at its analysis. Marubeni staffers sent to Westlake have learned about their data analytics – a big plus for us, and we want to leverage that in Indonesia, Chile and Australia – where Marubeni invests in finance business – and any new market in the future. ,” says Marubeni Auto Investment (USA) Holding CEO Seisuke Nakajima.

The Long Road Ahead

With nearly $10 billion in assets under management today, up from just $400 million a decade ago, Westlake is looking at its next major goal: $20 billion in assets by 2030. It’s already on pace to hit $13 billion by 2022, and the firm wants to build on its car loan expertise to expand into credit cards and personal loans, Anderson says.

Bret Hankey, Westlake’s vice chairman, says that Marubeni’s role will be key going forward. “With Marubeni’s resources and the relationship,” he says, “I think we have the chance to be the largest consumer auto finance company in the country.”

All information contained in this article is based on interviews conducted in August 2019.